Anti-Fraud Data Analytics Tests

The use of data analytics is a powerful fraud prevention, detection and investigation tool, and an important part of an effective and holistic fraud risk management program. According to the ACFE’s Occupational Fraud 2026: A Report to the Nations, organizations that use proactive data analytics as an anti-fraud control experience fraud losses that are 53% lower than organizations that do not use data analytics to combat fraud.

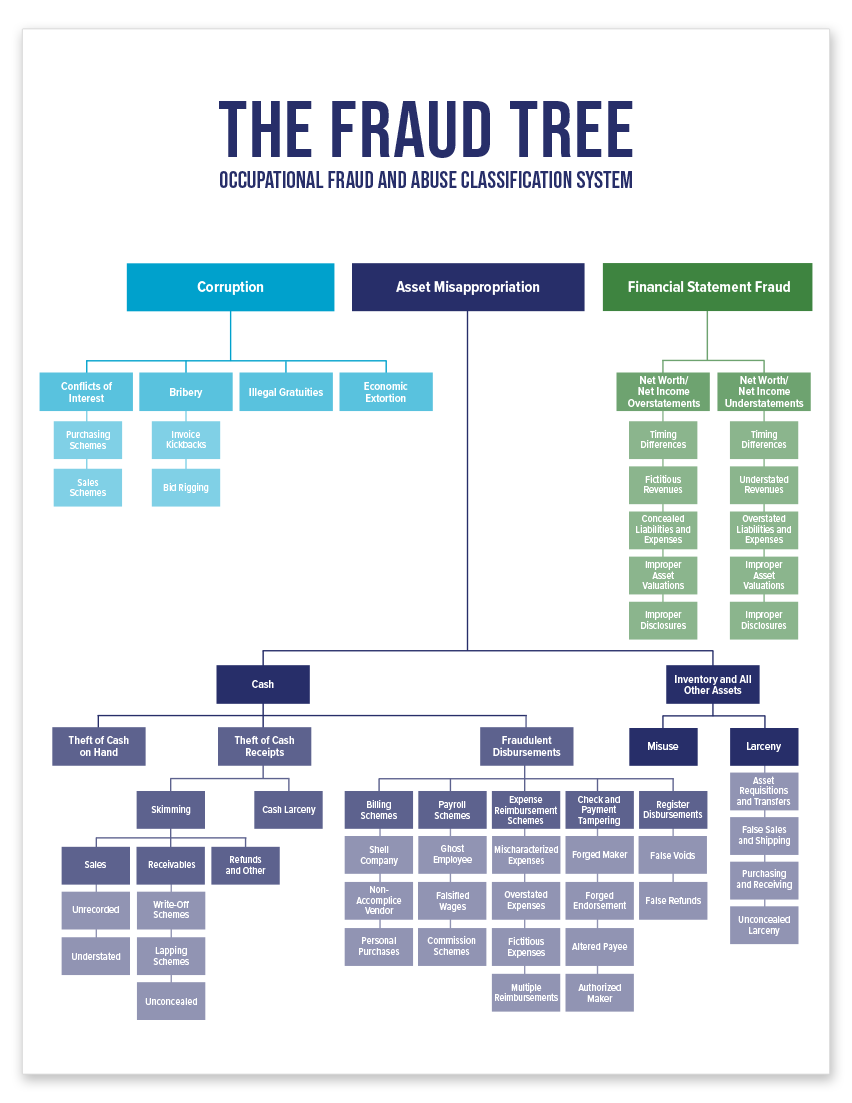

The interactive tool below provides you with numerous data analytics tests that can be used to help identify the red flags of various occupational fraud schemes. This tool is based on the structure of the ACFE’s Fraud Tree. You can drill down to a specific scheme type and see data analytics tests that are relevant to that fraud risk.

The ACFE would like to thank David Coderre for his contributions to the data analytics tests included in the interactive tool.

Corruption

-

Bribery

Kickbacks Data Analytics Tests

- Identify large expense reimbursements or petty cash draws/increases prior to obtaining a large contract.

- Analyze credits and free/discounted goods as a percentage of total sales by customer or distributor.

- Investigate cash payments to agents or customers, with a particular focus on round-dollar payment amounts.

- Analyze payments to out-of-country accounts.

- Identify payments to agents that are not located in the customer/sales regions.

- Analyze the free-text payment descriptions for high-risk keywords such as "expedite fee," "facilitation payment," or government liaison names.

- Analyze payments made for excessive travel, charitable donations, gifts, and entertainment.

- Analyze chart of accounts to identify vague or suspicious accounts where inappropriate payments could be expensed to, such as "miscellaneous expense," "special expenses," etc.

Bid Rigging Data Analytics Tests

- Review the number of bids submitted per contract and investigate sole-sourced or exceptionally low bids on contracts.

- Check for split contracts with vendors to identify orders that are below approval or bidding thresholds.

- Verify bidders and prices to identify fictitious bids.

- Investigate last-bid wins, bids that were altered last minute, and bids submitted after closing date.

- Compare ratio of contract awards to bids submitted by vendor and identify outliers.

-

Conflicts of Interest

Purchasing Schemes Data Analytics Tests

- Compare purchasing rates for similar products by vendor to identify if products were purchased at higher rates.

- Compare purchases by ordering clerk for each vendor and product to identify vendor preference patterns.

- Compare the total number of contracts by vendor to identify the presence of any bid-rotation activity.

- Determine the average value of contracts awarded per vendor to identify if high-dollar contracts are awarded systematically.

- Analyze whether any significant charitable and social contributions are linked to contract awards.

- Look for one-time vendors or vendors with expedited payments.

- Compare employee names, addresses, and account information to vendor master information to identify potential conflicts of interests or hidden relationships.

Sales Schemes Data Analytics Tests

- Compare sales prices and/or margins for products by customer to identify if products were sold at lower rates.

- Compare sales prices and/or margin by employee for each customer and product to identify any unusual pricing patterns.

- Analyze damaged good sales, credits, and returns by seller and identify outliers.

- Identify outstanding accounts receivable and analyze connection of respective customer information with known shell companies or sanctions lists.

-

Illegal Gratuities

Illegal Gratuities Data Analytics Tests

- Compare commission percentages by agent and/or region to identify outliers with significantly higher percentages.

- Identify contracts with fixed payments or unusual commission structures compared to all other contracts.

- Analyze commissions paid prior to sale to identify potentially inappropriate advances of bogus sales.

- Identify payments that are inconsistent with the contract terms.

- Investigate transactions related to missing contracts, contracts with gaps, or missing pages.

-

Economic Extortion

Economic Extortion Data Analytics Tests

- Analyze emails, social media, or online sources to identify common ownership or addresses.

- Analyze weekend activity of employees to identify misuse of information.

- Identify people accessing, downloading, and sending the organization's intellectual property to recipients outside of the company.

- Identify email contacts and associations to known shell or sanctioned companies.

- Analyze social media information to identify leaked insider information before official publication dates.

Asset Misappropriation

-

Cash

Theft of Cash on Hand Data Analytics Tests

- Reconcile cash on hand with balance in accounting and investigate any differences.

- Review the cash ledger for anomalous terms for cash usage or entries by unauthorized employees.

- Verify the segregation of duties for cash bookkeeping, bank reconciliation, and check-signer functions.

- Stratify payments by certain dollar amount and investigate groups, outliers, and round-sum amounts.

- Analyze cash reimbursements for travel and entertainment expenses by individual and compare to peers.

Skimming Data Analytics Tests

- Review sequential numbering of cash receipts journal to ensure no out-of-sequence numbers.

- Analyze cash as a percentage of total assets over time to detect skimming at a high level.

- Inspect for an employee bank account with a name similar to the company name.

- Inspect for alteration of the check payee or endorsement.

- Track the ratio of current assets to current liabilities over time to identify any anomalies.

- Identify higher-than-average uncollectible accounts.

- Extract invoices with partial payments.

- Summarize net sales by employee and extract top employees with low sales.

- Investigate customer complaints regarding payments not being applied to their accounts.

Cash Larceny Data Analytics Tests

- Compare listing of cash receipts submitted to cashier or accounts receivable bookkeeper to listing of deposit slips.

- Verify the linear relationship between sales, returns, and allowances over a relevant range. (Changes in this relationship may point to a fraud scheme unless there is another valid explanation.)

- Review the company's records of the numerical series of printed, prenumbered receipts, and verify that these receipts are used sequentially (including voided documents).

- Review the timeliness of deposits from location to location to the central treasurer's function.

- Compare adjustments to inventory to void or refund transactions summarized by employee.

- Inquire if individuals handling cash have taken vacation and analyze another employee's cash handling during that time.

Billing Schemes Data Analytics Tests

- Identify purchases made without respective approval or purchases made on an expedited basis.

- Review listing of unfilled or open purchase orders without any activity.

- Identify and investigate invoices that did not pass the three-way-match (purchase order, goods receipt, and vendor invoice) before the related liability was recorded.

- Verify that purchases are recorded in a purchase register or voucher register before being processed through cash disbursements.

- Identify payment terms on the purchase order that do not match the vendor master information.

- Extract vendors with incomplete profiles, especially those with missing telephone numbers or tax ID numbers.

- Match the vendor master file to the employee master file on various key fields, such as address or tax ID number.

- Identify duplicate purchase order numbers, credits, and invoices.

- Review payments with little or no sequence between invoice numbers.

- Identify disbursements in which the payment approval party is the same as purchase approval party.

Payroll Schemes Data Analytics Tests

- List employees with excessive overtime hours to identify irregularities such as more than 24 hours worked in a single day or significantly more hours worked than peers.

- Identify duplicate direct deposit numbers, employee names, addresses, or phone numbers.

- Identify persons on payroll with no time off for vacations or sick leave.

- Identify sudden, significant shifts in charging time by time series and pattern analysis.

- Map the employee addresses geographically and detect anomalies relative to their work location.

- Extract multiple payroll deposits to the same bank account in a single pay period.

Expense Reimbursement Schemes Data Analytics Tests

- Identify business travel with departures on Friday or Saturday and returns on Sunday or Monday and verify business purpose.Compare travel location and expense-incurred location.

- Isolate even-dollar amounts from unexpected sources (hotels, car rentals, etc.) and investigate for fraudulent expenses.

- Review expenses that always end in round numbers or with consistent amounts.

- Calculate standard deviation by expense type (i.e. meals, lodging, car rental, etc.) and investigate anything greater than two times the standard deviation from the mean.

- Stratify expenses by employee and job title/roles to identify outliers or inconsistencies.

- Identify expenses with missing required information such as dates, times, or purposes of expenses.

Check Tampering Data Analytics Tests

- Verify check number sequences, and identify missing check numbers that may indicate lax control over the physical safekeeping of checks. (Issue stop payments for all missing checks.)

- Compare checks made payable to employee names or to "cash" outside the normal payroll or expense checks. (Such disbursements could also uncover conflicts of interest, fictitious vendors, or duplicate expense reimbursement schemes.)

- Analyze the check register for duplicate check numbers or exact dollar amounts (to the penny) on the same date to different payees.

- Identify checks with no related system invoices.

- Identify purchases without purchase orders and summarize by vendor and issuer.

- Extract manual checks and summarize by payee and issuer.

Register Disbursements Data Analytics Tests

- Compare allowances by store to identify outliers.

- Summarize refunds by credit card number and compare to purchases.

- Calculate the number and amount of voids by sales clerk to identify outliers.

- Identify refunds for amounts greater than the selling price.

- Identify transactions with purchase and refund within 10 days or less.

-

Inventory and Other Assets

Misuse Data Analytics Tests

- Analyze differences in inventory count and identify higher utilization of materials or supplies.

- Compare stock turnover by product to expected turnover and investigate higher utilization.

- Profile supply usage or write-offs by month or department and identify outliers.

Larceny Data Analytics Tests

- Compare physical stock count with computed stock counts.

- Identify instances of disposal followed by reorder, which might indicate disposal/ theft of usable items.

- Summarize items sent to scrap or made obsolete by clerk.

- Stratify inventory adjustments by employee, extended cost, location, etc.

- Identify receipts per receiving reports in the receiving system that do not agree to the receipts per the accounts payable invoices.

- Extract inventory with a negative or zero price.

- Determine percentage change in sales, price, or cost levels by product and vendor.

Financial Statement Fraud

-

Fictitious Revenues

Fictitious Revenues Data Analytics Tests

- Compare discounts or incentives on a monthly basis to identify unusual spikes at the end of the quarter or year.

- Identify revenue recognized at period-end and subsequently reversed or partially reversed.

- Analyze gross margin by month and identify any outliers.

- Analyze sales to customers that have company names that sound like known customers and have missing fields.

- Analyze the emails of selected employees (accounting or sales) for revenue-recognition-related keywords indicating incentive/pressure, opportunity, and rationalization.

-

Timing Differences

Timing Differences Data Analytics Tests

- Analyze gross margin by month and identify any outliers.

- Compare invoice dates to shipping dates for large gaps in time or shipping date prior to invoice date.

- Compare incoming-invoice dates to goods-receipt dates for large gaps in time or shipping date prior to invoice date.

- Check any unusual revenue entries not supported by documents.

- Conduct a Benford's Law analysis to identify anomalies such as disproportionate number of invoices starting with specific numbers. (See: Benford's Law)

-

Concealed Liabilities and Expenses

Concealed Liabilities and Expenses Data Analytics Tests

- Compare and/or stratify expenses by month and to prior year and investigate outliers.

- Analyze expenses after significant cut-off dates to identify any delayed records.

- Analyze time of invoice to payment and identify invoices with unexpectedly short times between invoice and payment.

-

Improper Asset Valuations

Improper Asset Valuations Data Analytics Tests

- Review sales of fixed assets for prices significantly below or above depreciated value.

- Identify sales of fixed assets significantly before end of depreciation lifecycle.

- Review number of unplanned write-offs of assets that could indicate systematic issue in setting up depreciations.

- Isolate stock where cost is greater than retail price.

- Identify surplus or obsolete inventory.

-

Improper Disclosures

Improper Disclosures Data Analytics Tests

- Compare subsequent events to prior-year subsequent events.

- Compare related-party transactions to third-party transactions and reconcile to disclosure information.